What is an Employee Ownership Trust (EOT)?

An EOT is a special form of trust that holds shares in a company on behalf of its employees. It facilitates employee-ownership of a business, and the framework was introduced in 2014 as part of a government policy in support of this ownership model.

The government consulted in autumn 2023 on a number of potential changes to the operation of EOTs, but have yet to present the results of that review. The more notable proposals are covered in this note.

The key benefits of an EOT are:

- Employees can indirectly buy shares from the owners without using their own funds, providing a succession opportunity where there is no obvious third-party purchaser.

- There is no capital gains tax or inheritance tax payable on qualifying disposals of shares to an EOT.

- Employees can be paid income tax free bonuses of up to £3,600 (these remain subject to national insurance).

How is it different to an Employee Benefit Trust (EBT)?

An EOT is a specific type of EBT. An EBT is a trust that holds company shares on behalf of a class of beneficiaries.

EBTs are commonly used to acquire and hold shares that will be issued under employee share schemes, provide an internal market for shareholders in an unquoted company, or one of several other common purposes. An EOT has tighter requirements and a more specific purpose.

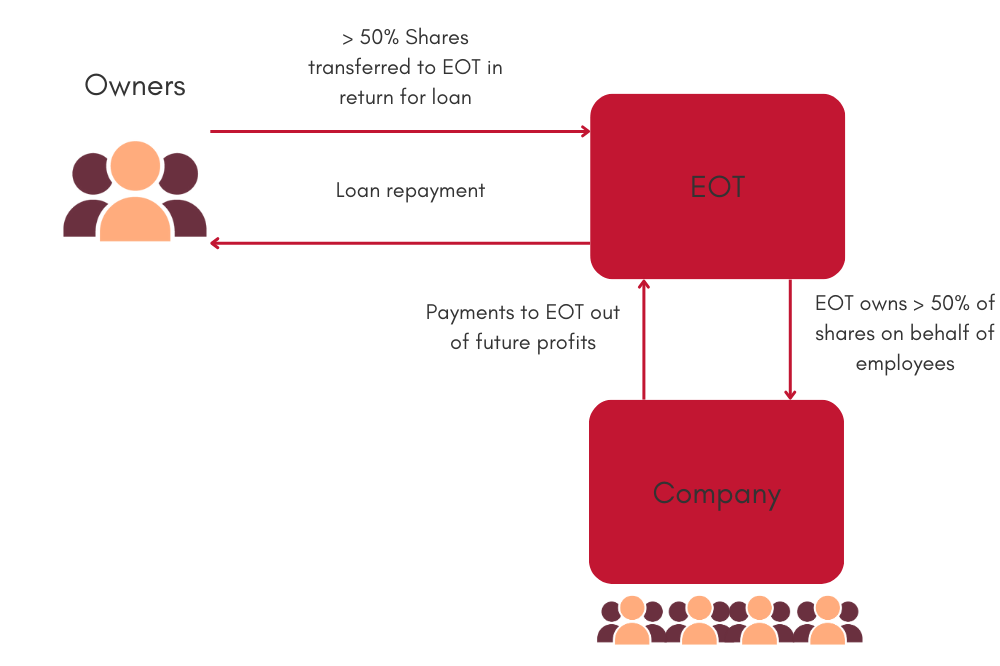

How does an EOT work and what criteria must be met?

An EOT is established in the following way:

- A trust is set up with a company as the trustee.

- The owner will sell their shares to the trustee company (at an external valuation) in return for a debt owed to the owners from the trustee company.

- The debt will be repaid to the owners out of future profits of the business (that are paid up to the corporate trustee), or in some circumstances using third party financing obtained by the business.

In order to qualify for the tax advantages, the following criteria must be met:

- Trading: The company must be a 'trading' company

- Control: The trustee must hold more than 50% of the share capital and voting rights in the company and be entitled to more than 50% of the profits available for distribution and assets on a winding up.

- All employees: The shares must be applied for the benefit of all eligible employees on the same terms (see Equality). Certain employees are excluded – broadly anyone who already holds or has held more than 5% of the shares in the company (or is a close family member of such a person).

- Equality: Differentiation from the 'same terms' is permitted only on the following bases: remuneration level, length of service and hours worked. Staff can be excluded for the first 12 months of service only.

What are the advantages for the current owners?

- An EOT can provide a mechanism to transfer ownership to employees if this is a motivation for personal reasons for an owner, or because there is a limited market for a third-party sale.

- No capital gains tax is payable on a qualifying sale of shares to an EOT (this does not apply to corporate shareholders). This provides a tax saving of up to 20% of the tax that may otherwise arise on the gain. The disposal is treated as a no gain/no loss disposal for capital gains tax, so if the company is sold by the EOT in the future the deferred gain would crystallise.

- The owners do not need to sell all of their shares and can continue to hold their position as directors of the business.

- There is no IHT payable on the transfer to the trust, or on an ongoing basis within the trust.

- If a business is currently operated in partnership, this can be incorporated in order prior to sale to meet the necessary criteria.

What are the benefits for the company and its employees?

The goals of the business are aligned with the employees and the model has been shown to increase employee retention and drive business growth.

The company can still issue share awards under existing or new plans.

The EOT can pay employees bonuses of up to £3,600 per year, free of income tax (these remain subject to national insurance). The company can take a corporation tax deduction for these bonuses.

What are the drawbacks and restrictions associated with EOTs?

As the sale price of the business is more commonly paid out of future profits, owners will receive their payment over a longer period than is usual with a third-party sale.

As a result, there is a risk that if the business does not continue to perform the full sale price may not be received.

If any of the qualifying conditions cease to be met in the tax year of disposal or the following tax year, the capital gains tax advantage will be removed.

How might the rules change in the future?

Given their increasing popularity, it is unlikely that we will see any meaningful change in the legislation surrounding EOTs, particularly with the Labour Party vocally in favour of employee ownership as a concept.

However, there are some proposals that the government could enact following a period of consultation that ended some time ago. These are intended to prevent what HMRC sees as potential abuses of the current rules.

The main points of interest are as follows:

- Former owners or connected persons would be prohibited from taking control of the company by controlling the EOT board.

- To require that the trustees must be UK residents.

- To require increased employee representation on the board of trustees.

- To allow for tax free bonuses to be awarded to employees without including directors.

It is the UK residency that may have the most widespread impact, particularly given that having offshore trustees can be commonplace, in the hope of ensuring that in the event that the company is sold by the trustees in the future, such a sale would not give rise to a UK capital gains tax charge for the trustees.

How can we help?

Whatever your circumstances we can advise on the suitability of an EOT as compared to other options, and if you decide to move forward we can guide you through the process, navigating commercial, contractual and tax issues.

Get in touch with one of our team below to find more.

Key contacts

Managing Associate

International Succession & Tax | Owner Managed Businesses | Private Wealth

Senior Associate - Trust Manager

Succession & Tax | Inheritance & Trust Disputes | Private Wealth

Related

Guides

11th July 2024

Guides

4th June 2024

Guides

Articles

Articles

5th January 2024

Guides

16th November 2023

Guides

29th August 2023

Guides

25th March 2021

Guides

21st June 2019